Home

+

Published : 08 Jan 2016, 02:08 AM

Bangladesh is one of the few countries which can brag about growing its foreign reserves. At the close of 2015, the accumulated foreign currency reserves hit a record high of $27.49 billion – sufficient to cover seven months of imports.

It is a tremendous confidence booster for a country which was described pejoratively as a "basket case", meaning hopeless within a few years of its birth as an independent nation. It was a cruel remark from the world's most powerful nation that opposed Bangladesh's independence. It was not only unfair, but also insulting for a nation struggling to overcome the trauma of a bloody liberation war and trying to rebuild a devastated economy in the midst of the worst global economic environment since the Great Depression.

Nevertheless, some who appreciated the challenge saw Bangladesh as a "test case", meaning "If development can succeed in Bangladesh, it can succeed anywhere else." And it did; from the testing ground of development, Bangladesh has become a centre in the whirlpool of development in less than three decades!

Should we be resting on our laurel of success that both defied the "doom-sayers" and surprised the "sympathisers"? No, instead, reserve accumulation should be an integral part of the country's development strategy. We should not only attract more foreign currencies, but also manage the reserve skillfully.

Reserve accumulation as self-insurance

In recent years, especially after the 1997-98 Asian financial crisis, countries have been accumulating reserves as "self-insurance" against potential external shocks often due to sudden outflows of capital or/and export slums.

Precautionary accumulation of foreign reserves for self-insurance purposes demonstrates lack of trust in the international financial architecture, led by the IMF. The global financial safety-net for countries experiencing sudden balance of payments crisis is found to be inadequate.

However, such reserve accumulation is not cost-less; it has opportunity cost. That is, reserves could have been used in a better way for development, especially in the social sector and infrastructure. The accumulated foreign reserves are normally kept in low-yielding US treasury bonds or in overseas bank account.

Thus, Bangladesh's reserves are in fact financing advanced countries!

But this is only part of the story. The build-up of reserves may also help to support countries' export-oriented development strategy.

Reserve accumulation as development strategy

More than their domestic resources, the lack of foreign exchange in sufficient quantity can be a binding constraint for many developing countries in their pursuit of development. This idea was formalised in the early 1960s as a "two-gap" model by Harvard Economist (later of the World Bank) Hollis Chenery and his associates. The lack of foreign exchange prevents importation of essential raw materials, technology and machinery to fully utilise domestic resources. This argument was used to justify foreign aid.

Later in the 1970s A.P. Thirlwall extended the idea that "in the long run, no country can grow faster than that rate consistent with balance of payments equilibrium on current account unless it can finance ever-growing deficits which, in general, it cannot". This provided the theoretical foundation for an export-led development strategy.

It seems Japan and East Asian countries have understood this quite well. Unlike many countries that used import licensing to overcome the balance of payments constraint, Japan, Republic of Korea and lately China chose export oriented development models.

Reserves accumulation allows countries to not only better manage and smooth capital flow cycles, but also maintain an undervalued currency through interventions in the currency market. Undervalued exchange rates can increase the competitiveness of export. The growth of exports, in turn, stimulates the economy, creating a virtuous circle of high saving and investment rates.

The use of an undervalued exchange rate to boost export oriented industries is better than the policy of sector- or firm-specific subsidies or interventions (e.g. licensing), which not only requires extra-ordinary bureaucratic ability to "pick the winners", but also is prone to rent-seeking. Consequently, reserve accumulations can have positive externalities on the production and industrial development, and can thus be a feature of a country's development model.

Reserve accumulation and faster growth

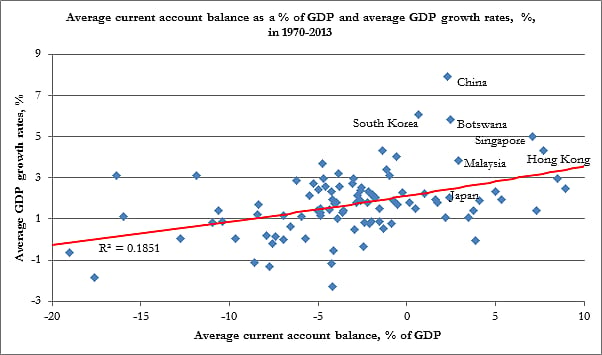

As shown in Figure 1, the relationship between the current account surplus and growth rates has been positive. All fast growing countries that were revelry called "miracle economies", from Botswana to China, had a considerably positive current account. Before the slowdown of growth since the mid-1980s, Japan looked very much like Botswana, Malaysia and Singapore – current account of over 2 % of GDP annually and growth of GDP per capita of over 4% a year in the 1950s-70s.

Figure 1: Average annual growth rates of GDP per capita and average current account balance, 1970-2013

Source: UN-DESA calculations based on World Bank World Development Indicators, IMF Balance of Payments; provided by Vladimir Popov.

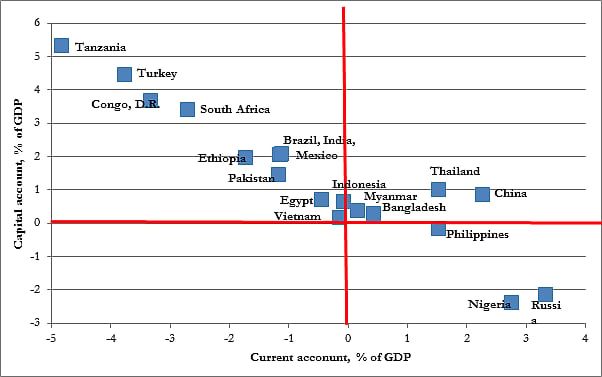

Central banks intervene in the foreign exchange market, keeping exchange rates from appreciating through building international reserves. China is the most often cited case, but a number of countries witnessed this phenomenon in some years, though only four large developing countries (with population of more than 50 million) – China, Bangladesh, Thailand and Myanmar – did so over a 15 year period (see Figure 2).

Figure 2: Average current account balance and capital flows to large developing countries (% GDP 2000-2014)

Source: IMF Balance of Payments; various years; provided by Vladimir Popov.

Countries in the upper left-hand quadrant of Figure 2 display the typical text-book phenomenon – current account deficits matched by capital account surplus. Countries (Nigeria and Russia) in the lower right-hand quadrant are suffering from resource curse; they have capital account deficits that are financed by current account surplus. When the current account surplus is not enough to finance capital outflows, forced devaluation of the currency occurs, often in the form of currency crises. The periodic overvaluation of their currencies caused by large foreign capital inflows associated with their resource sector, a typical case of "Dutch disease", implies the loss of competitiveness of their tradable sector.

Challenges of reserve accumulation

Although reserve accumulation and the use of an undervalued exchange rate is better than sector- or firm-specific export-oriented industry policy, it demands skill-full monetary policy management, supported by the fiscal authority. Otherwise, it can become self-defeating.

The accumulation of foreign reserves means an increase in the central bank's asset which has to be either matched by increasing in its liabilities or offset by reducing other asset items in a double entry book-keeping system.

One main liability item of the central bank is the currency in circulation. If that goes up as a result of foreign reserve accumulation, it will create inflationary pressure, which will offset the impact of exchange rate on exports.

The central bank, on the other hand, can reduce some of its asset items to offset the increase in foreign reserves. That is, it can off-load or sell some of the government bonds (debt) that it holds. This would lower the price of government bond and hence increase interest rates which can tackle inflationary pressure.

But higher interest rates will adversely affect domestic investment, including in the tradable sector. Higher interest rates may also attract more short-term foreign capital which may destabilise the domestic financial sector and create upward pressure on the exchange rate (i.e. taka may become stronger vis-à-vis dollar).

How to prevent the policy of reserve accumulation from becoming self-defeating? First, the central bank has to have sound capital flows management strategies to prevent both sudden surge of capital flows and capital flights out of the country. Many developing countries exercise control over capital flows (China and India would be prime examples).

Second, the foreign reserve accumulation strategy has to be supported by the fiscal authority. In practice, as the statistics shows, the accumulation of foreign exchange is financed through government budget surplus and debt accumulation by non-bank public. Therefore, it is highly important for the fiscal authority to enhance its revenue mobilisation capacity and efficiency. It must not borrow from the banking sector, especially the central bank. If it has to borrow, it must be from the non-bank public by making government savings certificate more attractive to the public using various non-interest fiscal measures. Most countries that accumulated reserves rapidly exhibited low inflation, and low budget deficit (or budget surplus), but increasing holdings of government bonds by the public.