Home

+

Published : 21 Nov 2024, 03:04 AM

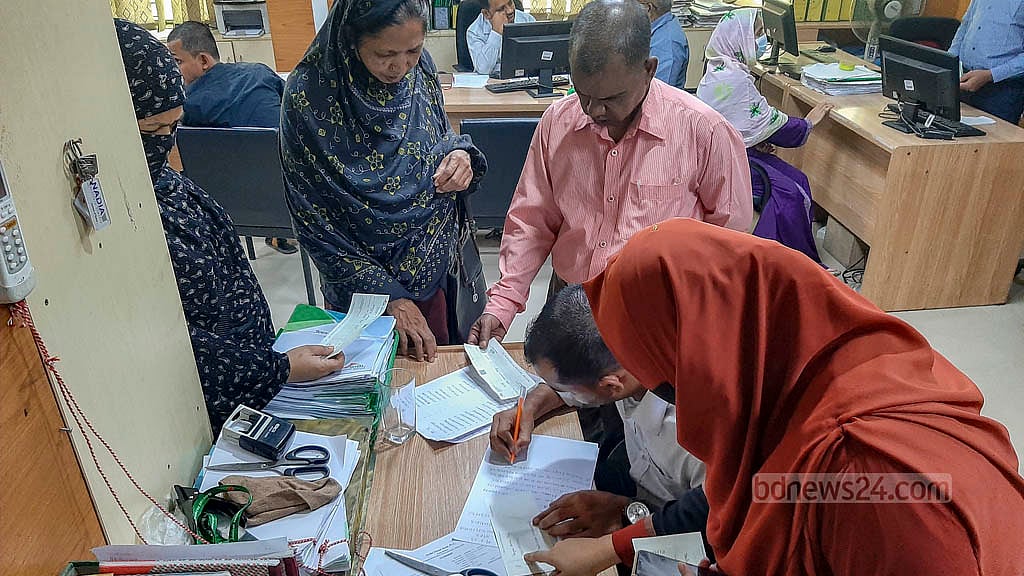

A lawyer in Dhaka took out a loan from a Shariah-based bank in exchange for a deposit in a fixed savings scheme. He transferred the loan amount into his daughter's account at the same branch. While he was initially able to withdraw about Tk 50,000, he is now struggling to access any funds.

At the Basabo branch of First Security Islami Bank, he is only allowed to withdraw Tk 5,000 per month.

The lawyer, who requested anonymity, said: “I needed the loan for an emergency, but since September, I have not been able to withdraw the money. Now, the bank is accepting a cheque for five thousand taka from the 19th to the 23rd of each month and giving out the money only on the 25th. The bank has limited withdrawals to just once a month.”

Even after meeting with the manager, he has not found a solution.

The bank manager told the lawyer, "You all know the situation. People are coming to withdraw together, and there's nothing we can do."

Although he cannot access his loan, the lawyer will still be charged interest on it, which adds to his anger and dissatisfaction.

His case reflects the predicament of millions of customers across the country, with many unable to withdraw their own money from some banks.

Even some bankers are struggling to withdraw their salaries, while employees of other organisations with salary accounts in these banks are facing difficulties in accessing their money.

In addition, a bank manager was filmed publicly crying after being unable to provide money to customers, with the video going viral on social media. Customers, unable to access their savings, have locked the bank doors in protest.

A bank's managing director, reportedly hiding, left several luxury cars outside his home. These unprecedented events have recently highlighted the deepening crisis within the banking sector.

A series of distressing incidents involving different banks has left customers from all walks of life deeply concerned.

As people repeatedly visit bank branches and leave empty-handed, public trust in the banking system is rapidly eroding.

In the wake of a government transition, Bangladesh Bank, the regulatory body for the banking and financial sector, has brought to light the struggles of several banks amid the shifting circumstances.

Under the ousted Awami League regime, widespread irregularities, fraud, and misuse of influence enabled the siphoning of money from banks and its laundering abroad.

When these misdeeds came to light, panic-stricken customers rushed to withdraw their savings, exposing the fragile state of several banks.

Analysts say the banking sector has been burdened by years of mismanagement. Despite decades of debate and criticism, no government has implemented effective reforms. Initially, state-owned banks, followed by private-sector banks, have become troubled due to non-performing loans and embezzlement, but the situation has not improved. Numerous initiatives have remained on paper, and theoretical discussions have continued for days, yet no positive outcomes have been achieved.

HOW BAD IS IT?

The banking sector continues to bear the brunt of mistrust following the fall of the Awami League government in the wake of the mass uprising. Even three months after the regime change, customers remain unable to withdraw funds from struggling banks— a situation not witnessed in recent years. This has raised questions about the fragile state of the sector.

While the visible signs of the crisis are evident, internal reports are revealing the deteriorating state of many banks. Alongside a liquidity shortage, several banks are burdened by bad loans,

while others are struggling with capital shortfalls. Although a few banks remain stable, the entire sector is now tarnished by the crisis. As more banks continue to weaken, the pressure on the Bangladesh Bank is mounting.

The central bank is not only working to stabilise struggling banks but also arranging funds to keep them afloat. As part of its liquidity support, the Bangladesh Bank provided Tk 60 billion to seven banks in the second week of November.

Among them, one of the country's largest banks, Islami Bank, reported a loss in the third quarter of the year. This marks the first time in recent years that the bank has faced a loss in any quarter. After a change in board control, EXIM Bank, which had benefited from the previous government's policies, also posted a loss for the September quarter.

In a recent meeting with the heads of 17 banks last Monday, Bangladesh Bank announced that any bank facing a capital deficit will not be allowed to distribute dividends.

According to regulations, banks with a capital shortfall cannot offer dividends. During the meeting, Governor Ahsan H Mansur reminded the attendees of this rule. Since most of these banks are listed on the stock market, this decision has impacted the stock market, leaving investors in a difficult situation due to the decline in share values.

Amid the turmoil of power changes, the boards of several banks have been dissolved and reconstituted. The new administration removed beneficiaries of the ousted Awami League government and brought back former partners or entrepreneurs to oversee the banks, while also appointing several independent directors to take charge.

Many bank entrepreneurs who benefitted from the previous government have been arrested, while others have fled abroad or gone into hiding. Reports have also surfaced about managing directors and top executives of several banks fleeing the country, going into hiding, or remaining absconded; they have stopped attending their workplaces since then.

Bankers and analysts say that the financial instability within several well-established banks, which once received a positive response from customers, as well as some new banks, highlights the current state of the banking sector. These facts and events reveal the fragility of the sector's financial condition.

They argue that a closer look at the country's primary financial sector will show that most of its key indicators are in poor condition.

The analysis of three key indicators — non-performing loans, liquidity crisis, and capital shortfall — signals a deteriorating condition. Added to this is the widespread lack of trust across all sectors, which most vividly reflects the dire state of the banking sector.

Governor Mansur highlighted the dire state of the banking sector during an event on the economy in the capital on Nov 11.

He said, “If a single family withdraws Tk 230 billion from a bank, what remains in that bank? In such cases, we need to do something new.”

He said that the weakness in the financial sector has left a significant impact on the country's economy, and the repercussions of the previous government's looting and money laundering are being felt now. Efforts are being made to recover from this crisis.

"We are now dealing with the aftermath of the past and engaging in corrective actions," he added while outlining steps being taken for the recovery of the banking sector.

HOW TO ASSESS THE CONDITION OF BANKING SECTOR

This year, Bangladesh Bank prepared a report titled "Banks Health Index (BHI) and Heat Map" to evaluate the overall condition of banks. The report revealed that nine banks, including four state-owned banks, are in the "red" zone, indicating a fragile financial situation.

In the report, 29 banks are in the "yellow" zone, and 16 banks are in the "green" zone.

Mohammad Ali, the managing director and chief executive officer, or CEO, of Pubali Bank, believes that several key indicators can determine the financial health of a bank. One of the most important indicators is the bank's overall liquidity position.

The CEO said, “We need to check whether the bank has sufficient cash on hand. The bank’s ability to maintain the Cash Reserve Ratio [CRR] and Statutory Liquidity Ratio [SLR] with the central bank after giving out cash to customers is a key indicator of its overall health.”

In addition, he believes that a higher deposit rate in a bank generally indicates a stronger financial position. According to him, increased deposits mean greater customer trust in the bank.

Ali added that the adequacy of the bank's capital and its ability to maintain provisions properly are considered crucial parameters when assessing a bank's health.

He identified non-performing loans as another key indicator.

A non-performing loan, or NPL, is a bank loan subject to late repayment or is unlikely to be repaid by the borrower.

If NPLs increase, a bank’s capital will be under pressure, and it will struggle to maintain proper provisions.

To assess the overall health of a bank, Bangladesh Bank regularly conducts the CAMELS rating, which evaluates the bank’s capital adequacy, asset quality, management quality, earnings, liquidity, and sensitivity to market risks.

This rating is confidential, and therefore not published, but reports suggest that in recent years, the number of poor-performing banks has ranged from 10 to 12, while 8 to 9 banks are considered to be in ‘fair’ condition, and others are seen as ‘satisfactory.’

A senior official of Bangladesh Bank told bdnews24.com that the number of poorly rated banks will likely increase further in the near future.

RECORD HIGH DEFAULT LOANS

The banking sector is currently grappling with its highest-ever level of non-performing loans, driven by widespread irregularities and fraudulent activities.

Reports indicate that not only have the loans not been repaid, but large sums have also been siphoned off.

The central bank’s latest data shows NPLs have increased by nearly Tk 740 billion in the July-September quarter, more than two and a half times higher compared to the previous three months. The total amount of NPLs has now reached Tk 2.8 trillion, accounting for 16.93 percent of the total loans disbursed. This marks a significant rise from Tk 2.11 trillion recorded at the end of June. State-owned banks hold the highest share of non-performing loans.

According to Bangladesh Bank, by the end of June, NPLs had surged to over Tk 2.11 trillion. This has pushed the ratio of classified loans to total loans to 12.56 percent. At the end of March this year, the figure stood at Tk 1.82 trillion, or 11.11 percent of total loans distributed.

Zahid Hussain, former lead economist at the World Bank’s Dhaka office, believes that state-owned banks are facing significant challenges, including both non-performing loans and capital shortages.

He said powerful individuals and groups had borrowed large sums from these banks and failed to repay them, which has severely weakened the financial condition of these banks.

“These state-owned banks are grappling with two major issues—capital shortfall and non-performing loans. Although these banks are not impacted by liquidity issues due to their state ownership, they are suffering from a capital deficiency, with over 50 percent of loans classified as non-performing,” the economist said.

The total non-performing loans in private banks amount to Tk 999.21 billion, which is 7.94 percent of their total loans.

Bankers claim that out of over 60 banks, only about 10-12 are in a strong position, while the majority are grappling with either default loans or liquidity crises, and some are facing severe capital shortages.

CAPITAL DEFICIT AT CRITICAL LEVELS

According to data from Bangladesh Bank, several state-owned banks—including Agrani, Janata, Basic, and Rupali—are facing capital shortfalls.

Among the specialised banks, both the Agriculture and Rajshahi Krishi banks have long been struggling with capital deficiencies.

The list of private banks dealing with capital deficits is also long. These banks have been operating for years, often bypassing regulations and securing exemptions from Bangladesh Bank, allowing them to continue business without properly resolving their capital deficiencies.

Bankers pointed out that for years, most state-owned banks have been running without adequate capital. To relieve the crisis, the government had provided these banks with capital injections amounting to billions of taka, using public funds from taxpayers. Despite these capital infusions, these banks have been unable to overcome their capital shortfalls. Over time, many private banks have also been added to this list.

An increase in NPLs contributes directly to the worsening capital shortfall. As NPLs rise, banks are required to set aside more provisions or reserves to cover the risk, which places further strain on their capital.

![]()

The provision system is put in place to safeguard the health of banks and protect the interests of depositors. In the case of defaulted loans, banks try to mitigate the situation by maintaining cash reserves at the central bank. However, by setting aside excessive provisions, many banks ultimately fail to maintain the required capital.

LIQUIDITY CRISIS

Economists and bankers agree that the biggest challenge currently facing the banking sector is the liquidity crisis. The problem has become particularly acute in Islami Shariah-based banks, with the root cause lying in the large-scale money outflows from banks controlled by the Chattogram-based S Alam Group during the tenure of the ousted Awami League government. These banks are struggling to return regular deposits to their customers.

Before the government change, Bangladesh Bank had provided special arrangements for these banks to receive cash. However, after the fall of the Sheikh Hasina regime, these Shariah-based banks, along with many others, have been unable to pay their customers on time. Reports of customer dissatisfaction, protests, and bankers facing hardships have surfaced.

Bangladesh Bank intervened to help these banks by acting as a guarantor, arranging cash from other banks to relieve their liquidity crisis. Several rounds of funds have been provided in an attempt to stabilise the situation, but the banks are still struggling to meet customers' demands. Even bank staff and employees of other institutions are finding it difficult to withdraw their salaries. These banks' branches, scattered across the country, are also failing to attract deposits.

Zahid said, "The situation of these Shariah-based banks is so bad that calling it 'bad' would be an understatement. These banks are being kept alive on life support in the ICU."

Following fall of the Sheikh Hasina regime, fears spread that banks could close, particularly those controlled by Saiful Alam [S Alam Group], which were linked to large-scale irregularities and money laundering. Amid rumours of imminent closure, customers rushed to withdraw their deposits, causing banks to fail in meeting withdrawal demands.

However, by September and October, money that had left the banking sector began to return. Customers who had withdrawn funds from weak banks and deposited them in more stable ones, as well as those who had kept cash at hand, began to re-deposit their money.

According to Bangladesh Bank's data, Tk 42.09 billion had returned by October.

Sheikh Mohammad Maroof, managing director of the Dhaka Bank, views this as a positive sign for the sector.

"The reason for this return is that customer confidence is gradually improving," he said.

CUSTOMER CONFIDENCE AT ROCK BOTTOM

Amid growing concerns over irregularities in the banking sector, a US-based expatriate instructed a relative in Dhaka to visit the branch of his bank to check on his account. For over 20 years, tenants of his flat had been depositing rent into this account, with the funds largely untouched and accumulating into a large sum, sparking heightened anxiety.

The branch manager informed the relative that withdrawing the entire amount at once would not be possible. Despite attempts to explain the situation to the expatriate account holder, the manager eventually agreed to allow Tk 50,000 withdrawals weekly.

However, the expatriate lost faith in the system and decided to withdraw his funds entirely. For two months, he has been withdrawing small sums weekly and transferring them to another bank. Many other customers, facing similar distrust, are shifting their deposits from one bank to another.

This growing mistrust has led many customers, like him, to withdraw funds from one bank and deposit them elsewhere. Observing this trend, Bangladesh Bank spokesperson Husne Ara Shikha, has called on customers to avoid such actions and maintain confidence in the banking system.

At a press conference on Nov 6, she said: “The surge in customer visits to banks has made it challenging to meet withdrawal demands. The number of customers withdrawing funds is considerably higher than before. Bangladesh Bank is committed to rebuilding trust in the banking system. Maintaining depositor confidence is a shared responsibility of both the banks and the central bank.”

Islami banks, particularly those under the ownership of S Alam Group, have faced the most pressure, compounded by cash shortages at several other troubled banks. In some branches, customers were unable to withdraw more than Tk 10,000 last week, while other branches ceased withdrawals altogether.

This situation has persisted for over four months, leading to widespread distrust among customers, according to bankers.

Abdur Rahim, a customer of Social Islami Bank’s Dohar branch, shared his ordeal on Thursday. Despite repeated visits throughout the past week, he was unable to withdraw Tk 30,000.

"When I visited the Dohar branch, they directed me to the Motijheel branch due to insufficient funds. But here too, I am being denied my money. They say I must collect it from my original branch. My relative is hospitalised—how will I get the money now? Why should I endure this for my own funds?” he said.

Mohammad Motaleb, manager of the principal branch in Dilkusha, explained that cash withdrawals have surged while deposits have dwindled, leading to severe liquidity constraints.

NOT ALL BANKS IN CRISIS

Despite the evident vulnerabilities in the financial sector, not all banks are in distress. A handful of banks remain in a stable position, even as they feel the ripple effects of challenges faced by others. Of the 61 active banks in the country, only a few maintain solid footing.

Economist Zahid said, “It would be an oversimplification to say that the entire sector is failing. A large portion of the banking sector is indeed grappling with major issues, but there are exceptions.”

Bankers point out that rising interest rates on deposits and loans have placed even well-performing banks under strain. The cost of acquiring deposits has increased, but a decline in investments has reduced loan demand from entrepreneurs and industries.

In addition, the central bank's contractionary monetary policy has curtailed credit flow, impacting even strong banks. Consequently, many banks are experiencing reduced earnings.

DOLLAR MARKET INSTABILITY, HIGH INTEREST RATES

For more than two years, the instability in the currency market has slightly eased in recent months, but the price of the US dollar, the primary currency for foreign transactions, remains high. The demand for dollars is still unmet, with both businesses and the government struggling to obtain the necessary foreign exchange for outstanding payments. This ongoing shortage has resulted in a decline in business and created a negative atmosphere surrounding banks for some time. The entire sector has been impacted.

In May this year, when Bangladesh Bank introduced the ‘crawling peg’ system, the dollar rate jumped by Tk 7, reaching Tk 117. As the price of the dollar rose in banking channels, remittance inflows increased. From August to October, remittances exceeded two billion dollars for three consecutive months. There has been a slight recovery in expatriates' trust in sending money through banks. However, this surge in remittances has not benefited the banks that are facing difficulties.

Syed Mahbubur Rahman, managing director and CEO of Mutual Trust Bank, views the growing remittance trend as a positive development for the entire sector. He believes that the distrust that had plagued the banking sector is gradually fading. However, he emphasised the urgent need for reforms in several areas.

HOW WILL THE CRISIS BE RESOLVED?

The banking sector in Bangladesh has been grappling with various issues for a long time, with previous governments discussing potential solutions to the sector's problems. Though steps like the formation of reform commissions and task forces were suggested, there has been little change in the situation. In fact, over time, the situation has worsened.

Economist and researcher Zaid Bakht, who served as the chairman of the state-owned Agrani Bank, states that overcoming the banking sector's crisis requires a long-term plan. He emphasises that immediate steps must be taken in line with that plan. A major issue is the growing volume of non-performing loans. Identifying the defaulters and bringing them to justice is critical, with efforts to recover as much money as possible from them.

"According to Bangladesh Bank’s regulations, the issues within each bank must be addressed. The government should offer full support to Bangladesh Bank so it can take the necessary steps,"he added.

BANKING, CAPITAL MARKET, TAX REFORMS MUST BE PRIORITISED: SALEHUDDIN

The interim government set up a task force to address the long-standing crisis in the financial sector. They also proposed the formation of a banking commission.

Economic Advisor Salehuddin Ahmed assured the public on Tuesday that despite management weaknesses and irregularities causing problems in several banks, none of these banks would be closed.

He said, “We are currently taking reform measures based on symptoms. Some banks have the potential to recover, including the largest bank, Islami Bank, which is on the path to recovery. Some banks may continue to struggle, but we will not shut them down. We are determined to leave a legacy of progress, ensuring that the reforms we implement pave the way forward.”

[Writing in English by Sheikh Fariha Bristy]